.png "Wealth Conservatory Logo (1)")

.png?width=440&height=102&name=Wealth%20Conservatory%20Logo%20(1).png)

Loans and credit cards all sound like a dream come true when you first hit some level of financial awareness. Many young adults have thought, “Am I about to be handed free money?” That’s before they have a true understanding of what it means to be in debt.

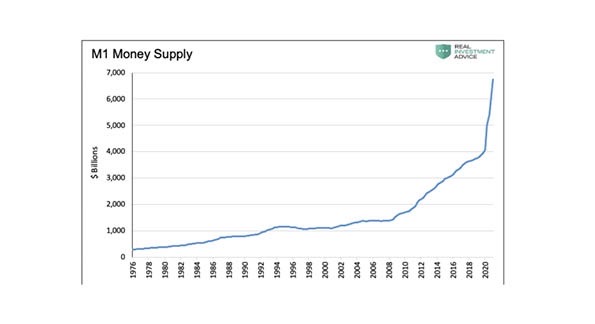

Conventional economics tells us something that would seem to be obvious: when the government creates more money, there is more money available to buy things, and therefore the prices of things rise—and we get inflation. For some reason, this logical sequence of events seems not to be happening today. The amount of money in the U.S. economy is 25% higher than it was at the start of 2020—the fastest pace of growth since the U.S. Federal Reserve banking system was established in 1913. You can see from the chart that we have experienced steady growth of the money supply until around 2009, when the slope increased (remember the Great Recession?), and then in early 2020 the growth of dollars in the system made another dramatic shift upwards.

If you could live in any U.S. state, which one would let you keep more of your money than others? The answer turns out to be surprisingly complicated…

The initials ESG refer to the factors used to measure the environmental and ethical impact of investing in a company. The “G” stands for governance, corporate governance to be exact. A trend within the group of investors who care about the systems, structures and policies governing a corporation is investing in more women-owned and women-led businesses.

The wide world of investment is full of opportunities. Unfortunately, along with these opportunities comes a lot of jargon and confusion. Common questions that people ask themselves are “What are mutual funds?” and “Should I invest in mutual funds?” Like most things in life, there are pros and cons to doing so. This breakdown will cut through the buzzwords so that you can get a better idea of what mutual funds are and whether or not investing in them is a good financial fit for you.

You may have read that the U.S. Federal Reserve Board, which has unlimited financial resources, is now buying ETFs. With the Fed’s $4.75 trillion in assets significantly larger than your own retirement portfolio, it seems fair to ask: does it make sense for a government agency to be buying investments alongside retail investors?

The Coronavirus Aid, Relief and Economic Security (CARES) Act was enacted on March, 27th. It is intended to be federal government support in the wake of the coronavirus public health crisis and associated economic fallout. The CARES Act is built on the two former pieces of legislation and is meant to provide more robust support to both individuals and businesses, including changes to tax policy. Here are 8 aspects of this pandemic relief measure that are important to take note of…

Investors of a certain age, with long memories, remember the prelude to the Tech Wreck of 2000. Back then, even investors in the supposedly diversified S&P 500 index of 500 stocks discovered that they were 33% invested in technology. By 2003, after a murderous series of downturns that saw a number of tech companies go out of business, that weighting had fallen back to 14% of the index.

Every year, we hear from market prognosticators telling us where the market will be a year from now, the future direction of interest rates and when the economy will or won’t go into recession. But does anybody ever keep track of the accuracy of these forecasts?

You may be aware that on December 20, President Trump signed something called the SECURE Act (Setting Every Community Up for Retirement Enhancement) into law. But what does that mean for financial consumers? Among other things, the new law increases the tax credit for small businesses to set up new retirement plans for their employees, from $500 to $5,000. It allows small employers to automatically enroll their employees and allows smaller companies to create multiple employer plans with other companies in the area, reducing the obstacles to offering 401(k) and other retirement plans. A great deal of insurance industry lobbying support went into another provision that requires all qualified plans to show participants how they can convert their existing balances into “lifetime income” through an annuity.

One of the oddities about the American financial marketplace is how so many consumers prefer to keep their assets at the large Wall Street firms. This is odd because these firms famously have sales cultures driven by multi-million-dollar bonuses for their brokerage sales agents and whose BrokerCheck reports read more like rap sheets than profiles. (Don’t believe us? Type a famous brokerage firm name into the second box in the BrokerCheck website—https://brokercheck.finra.org/—and you’ll get hundreds of thousands of listings of specific broker transgressions, fines, and examples where customers received arbitration awards after various kinds of financial abuse.)